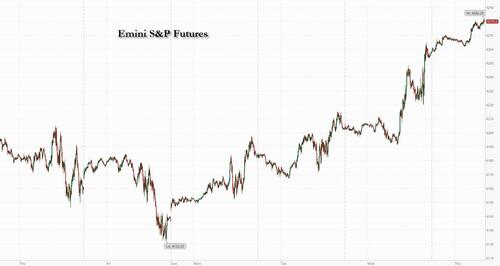

US equity futures, and global stocks and bonds extended gains Thursday as traders bet the Federal Reserve is ending its historic tightening campaign, and that easing may not be too far behind. As of 8:00am, S&P 500 futures rose 0.5%, while Nasdaq 100 futures gained 0.7%. Both underlying indexes had jumped on Wednesday after the Fed held interest rates steady and the Treasury announced plans to slow the pace of increases in quarterly long-term securities sales. The dollar weakened and Treasuries steadied after sharp gains following Powell’s comments yesterday. In Asia, the yen extended its gains from Wednesday, while the South Korean won led emerging-market currencies higher. The 10-year TSY yield dipped two basis points after falling below 4.75% for the first time in two weeks. Elsewhere, the latest major company earnings also provided a dose of good news.Commodities are mixed with WTI adding 1.5% in the morning while base metals are for sale. Today, macro calendar is quieter: we have some second-tier labor data (Challenger Job Cuts, Nonfarm Productivity, ULC) and Factory Orders. We will receive AAPL’s earnings after the bell. All eyes on Friday’s NFP and ISM-Srvcs releases.

In premarket trading Starbucks rose after sales surpassed expectations. Novo Nordisk A/S rose after reporting that third-quarter sales surged amid the frenzy for its blockbuster obesity and diabetes drugs. Shell Plc gained after accelerating the pace of share buybacks as its third-quarter profit rose. Solar stocks fell after solar equipment-makers SolarEdge and Sunrun plunged after missing 3Q sales estimates. Apple headlines the roster of US earnings due later. Here are some other notable pre-market movers:

- Airbnb shares drop as much as 2.2% after the online travel company forecast revenue for the fourth quarter that missed the average analyst estimate. The short-term rental platform cited “greater volatility” in the economic environment that will in turn slow demand for travel.

- Confluent slump more than 30% after the software company narrowed its total revenue guidance for the full year, missing the average analyst estimate. Analysts noted that the company’s cloud business was hit by two large customers paring back spending.

- DoorDash shares jump 11% after the online food-delivery company third-quarter results beat expectations and its outlook was viewed as strong by analysts.

- Elf Beauty shares surge 14% after the cosmetics brand beat adjusted EPS estimates in the second-quarter and boosted full-year guidance for the metric above consensus expectations.

- Etsy shares fall 5.2% after the e-commerce company reported its third-quarter results and gave a forecast. The company said gross merchandise sales for the fourth quarter are “currently estimated to decline in the low-single-digit range on a year-over-year basis.”

- Fastly shares jump 18% after the infrastructure software company narrowed its adjusted loss-per-share forecast for the year. Analysts noted solid execution amid a challenging environment.

- PayPal shares rise as much as 7.8%, on track for their biggest gain in nearly a year, after the digital and mobile payments company reported third-quarter results that beat expectations across key metrics.

- Qualcomm shares gain 5.7% after the chipmaker reported third-quarter results that beat expectations and gave an outlook that is seen as strong. Analysts noted that its mobile inventory was largely cleared.

- Roku shares jump 19% after the streaming-video platform company reported third-quarter results that beat expectations on key metrics and gave an outlook analysts see as positive.

While the Fed left the door open to another increase after pausing Wednesday, officials hinted that a run-up in long-term Treasury yields reduces the impetus to tighten policy further. The Bank of England algo kept interest rates unchanged at the highest level since 2008 amid evidence that the UK economy, labor market and inflation are weakening.

Fed Chair Jerome Powell on Wednesday noted that financial conditions have “tightened significantly in recent months driven by higher, longer—term bond yields, among other factors.” He repeatedly said the committee was moving “carefully,” a wording that often has signaled a low likelihood of any immediate change in policy, while adding that risks to the outlook have become more two-sided as the tightening campaign nears its end.

“The Fed did not throw in the towel yesterday, but the changes in the speech are in line with a more moderate growth situation,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “What transpires from the speech is essentially a first eyebrow raised at the real growth situation, which markets decided to take for a ‘bad news is good news’ message.”

US yields were already heading lower prior to the Fed decision after the government announced plans to borrow slightly less than expected over the next three months, reassuring investors worried about a deluge of debt issuance.

The dual statements from the Treasury and Fed helped reverse some of the steep declines in US government debt and the S&P 500 over the last three months. The US stock gauge has now climbed for three days in a row, and strategists including at Barclays Plc said the bar for a further rally was low on wagers of a peak in rates as well as supportive year-end seasonal trends.

Optimism that central banks have come to the end of their rate hiking campaign fueled gains in Europe, led by rates-sensitive real estate stocks. The Stoxx 600 is up 1.4%, rising for a fourth day, with real estate and technology shares leading gains. Here are some of the biggest European movers:

- Novo Nordisk shares rise as much as 3.2% after the firm reported Wegovy sales for the third quarter that beat the average analyst estimate

- Shell shares rise as much as 2.5% in London after the oil major’s results met expectations, providing investors with some relief after recent disappointments at peers

- BT shares gain as much as 7.6% after the telecom operator raised free cash flow guidance to the higher end of a previous range, noting a fall in capital expenditure and per-unit fiber build costs

- Tenaris rises as much as 10%, the most since February, after the steel producer reported third-quarter Ebitda that beat estimates, with analysts also positive on the Italian pipe and tube manufacturer’s $1.2b buyback plan and increased dividend

- Fortum rises as much as 7.8%, the most since December, to lead gains in the Stoxx 600 Utilities Index after reporting Ebit the third quarter that beat the average analyst estimate

- Hugo Boss shares jump as much as 5.9%, lifting the broader luxury sector, after its third-quarter results beat expectations. By sticking to its prior guidance, the high-end fashion retailer sends a reassuring message on luxury demand, RBC analysts note

- Adecco shares jump as much as 14%, the most intraday since March 2020, after the Swiss staffing company reported third-quarter profits that beat expectations

- Geberit shares gain as much as 12%, the most since October 2008, after the Swiss building materials firm’s Ebitda growth beat estimates. Analysts note the otherwise challenging environment and positive margin development

- ING shares fall as much as 4.8% after the lender’s miss in net interest income overshadowed a better-than-expected share buyback program of €2.5 billion

- Swisscom shares fall as much as 4.7%, the most in three months, after the telecom operator’s 3Q results showed a deepening service-revenue decline in its home market

- Haleon shares fall as much as 4.7%, the most since March, after the consumer-health company reported sales volume in the third quarter that lagged behind expectations

Earlier in the session, Asia stocks rallied on signs the Federal Reserve may be done with its tightening cycle, with heavyweight tech shares getting an added boost from Advanced Micro Devices’ strong sales forecast. The MSCI Asia Pacific Index climbed as much as 1.7%, headed for its best day since July 13. TSMC, Samsung Electronics and Alibaba were among those that contributed most to the benchmark’s gain. All major markets were in the green, mirroring the advance in Wall Street after the Fed held off on raising interest rates for a second meeting and Chair Jerome Powell noted officials are “proceeding carefully.” Traders who were bracing for a hawkish hold cheered the remarks. Futures were pricing in a roughly one-in-four chance of another rate hike by January, compared to around 40% the day before.

- Shares in mainland China barely rose to underperform the region, after another substantial PBoC liquidity drain with mixed signals on its economic recovery. The Hang Seng benchmark was boosted by a surge in tech and strength in property.

- Japan's Nikkei 225 briefly climbed above 32,000 with the biggest movers driven by earnings and automaker updates.

- ASX 200 was higher with gains led by notable outperformance in tech and real estate amid a drop in yields.

- Indian stocks rose in line with other Asian peers as the Federal Reserve’s signal that it may be done with rate hikes spurred a risk-on rally in global equities. The S&P BSE Sensex rose 0.8% to 64,080.90 in Mumbai, while the NSE Nifty 50 Index advanced by the same magnitude. The Nifty Realty Index closed 2.5% higher.

In FX, the Bloomberg Dollar Spot Index fell 0.4%, extending a decline against its Group-of-10 peers as US yields fell after Fed Chair Jerome Powell hinted the US central bank may be done with hiking rates after it stayed on hold Wednesday. The pound is up 0.3% versus the greenback, lagging behind most of its G-10 peers ahead of the BOE rate decision.

In rates, Treasuries were slightly higher, with yields down across the curve, adding to Wednesday’s session gains spurred by the Treasury’s refunding details and Fed Chair Jerome Powell’s press conference. In London session, gilts have outperformed bunds as money markets pare BOE tightening premium and add to rate-cut wagers ahead of the BOE policy decision at 8am New York. US yields richer by up to 3bp across long-end of the curve, which outperforms, flattening 5s30s, 2s10s spreads by 1bp and 3bp on the day; 10-year yields around 4.705% and near bottom of days range into early US session.

In commodities, oil prices advance, with WTI rising 1.3% to trade near $81.50, after sliding around 5% over the previous three sessions. Spot gold gains 0.3%.

Bitcoin is in little changed on the session after once again eclipsing the $35k mark in Wednesday's session; since then BTC has experienced relatively steady trade and holding around the USD 35.4k mark towards the mid-point of its USD 35.09-35.962 range as it failed to breach the USD 36k mark in APAC trade.

Looking to the day ahead now, one of the main highlights will be the Bank of England’s latest policy decision and the subsequent press conference where we’ll hear from Governor Bailey. Otherwise, central bank speakers include the ECB’s Lane and Schnabel. Data releases from the US include the weekly initial jobless claims and September’s factory orders, whilst there’s also German unemployment for October. Finally, today’s earnings releases include Apple and Starbucks.

Market Snapshot

- S&P 500 futures up 0.6% to 4,280

- MXAP up 1.4% to 154.38

- MXAPJ up 1.6% to 479.79

- Nikkei up 1.1% to 31,949.89

- Topix up 0.5% to 2,322.39

- Hang Seng Index up 0.8% to 17,230.59

- Shanghai Composite down 0.5% to 3,009.41

- Sensex up 0.7% to 64,026.18

- Australia S&P/ASX 200 up 0.9% to 6,899.73

- Kospi up 1.8% to 2,343.12

- STOXX Europe 600 up 1.2% to 441.60

- German 10Y yield little changed at 2.73%

- Euro up 0.3% to $1.0597

- Brent Futures up 1.4% to $85.79/bbl

- Gold spot up 0.2% to $1,986.37

- US Dollar Index down 0.45% to 106.40

Top Overnight News

- Japan’s Fumio Kishida is staking the future of his premiership on a $113bn stimulus plan centered on tax cuts and cash handouts, as he seeks to tackle the fallout from high inflation and record-low approval ratings. FT

- South Korea’s CPI overshoots the Street consensus in Oct (with core coming in at +3.2% vs. the Street’s +3.1% forecast). RTRS

- Preparations are in full swing for a summit between Xi Jinping and Joe Biden this month, but analysts say they do not expect any breakthroughs given the long-standing issues looming over the talks. They say the much-anticipated meeting could, however, bode well for US-China ties and send a positive signal to regional countries that the world’s two biggest economies are managing their differences and trying to ease tensions. SCMP

- China’s biggest memory-chip maker has had to raise billions of dollars in fresh capital, after burning through $7bn in funding over the past year trying to adapt to tough US restrictions on its business. Yangtze Memory Technologies Corp, which last December was added to a trade blacklist and prohibited from procuring US equipment to manufacture chips, exceeded its target for a new round, according to four people familiar with the situation. FT

- Hamas said 600 more foreigners, including 400 American citizens, are expected to leave Gaza today. Joe Biden said Israel and Hamas, designated a terrorist group by the US, should “pause” fighting to allow time to free more hostages. BBG

- Toyota announces plans to increase compensation for nonunion US factory workers days after the Detroit 3 struck deals w/the UAW. RTRS

- Speaker Johnson talks about a short-term spending bill that would fund the gov’t through Jan 15 with an eventual 1% cut to spending (Johnson expressed support for funding both Ukraine and Israel, but not in the same bill). Politico

- Jamie Dimon told Yahoo that another 75 bps of hikes are still possible. Dimon also warned that Texas risks hurting its business-friendly reputation with laws designed to punish Wall Street banks for limiting work with the gun and fossil fuel industries. BBG

- The iPhone 15 is in the spotlight when Apple reports postmarket. Results may show it’s off to a solid start, though investors will focus on the China outlook given weak early sales. BB

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly followed suit to the gains on Wall St where the major indices were lifted by soft data releases and after Fed Chair Powell’s post-FOMC press conference spurred a dovish reaction as he poured cold water over the September dot plots which had pointed to one more hike by year-end. ASX 200 was higher with gains led by notable outperformance in tech and real estate amid a drop in yields. Nikkei 225 briefly climbed above 32,000 with the biggest movers driven by earnings and automaker updates. Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark boosted by a surge in tech and strength in property, while the mainland lagged after another substantial PBoC liquidity drain.

Top Asian News

- BoJ Governor Ueda will stick to a pattern established, to move gradually toward an exit while maintaining the dovish rhetoric of his predecessor, via Reuters citing sources familiar with the BoJ's thinking. Given the uncertainty on the economic outlook, the BoJ will probably want to wait until at least Spring 2024 to normalise policy. If so, it makes sense to keep guidance dovish. Gradualism, if possible, is the preference. Next focus is ending NIRP and pushing short-term rates to 0 from the current -0.1%; the timing for a move is likely around Spring, when there will be clarity on annual wage negotiations. Do not want to get markets too excited about the likelihood of an early lift-off, given the numerous hurdles to clear. The most likely scenario of an exit, given the cost of a spike in market rates is seen as too high, would be to end YCC and negative rates but to give a loose pledge to intervene if bond yields rise abruptly.

- Japan's PM Kishida says he will prod firms to attain wage hikes next year that surpass those this year; a robust economy is the foundation of all key policies.

- China's regulators reportedly probe liquidity stress that sent rates to 50%, via Reuters citing source; asking institutions why they borrowed at very elevated rates.

European bourses are in the green, Euro Stoxx 50 +1.6%, in a continuation of the post-Powell/Fed trade. Sectors are all in the green with Real Estate, Tech & Construction benefitting from yields while Travel & Leisure lifts after strong Lufthansa comments. Elsewhere, Delivery names benefit from the main takeaway of DoorDash's numbers.

Stateside, futures reside in the green but with action slightly more contained than Europe as the region has already had a chance to react to the Fed, ES +0.4%; NQ +0.7% continues its outperformance amid ongoing yield action ahead of Apple earnings after-hours.

Top European News

- European bourses are in the green, Euro Stoxx 50 +1.6%, in a continuation of the post-Powell/Fed trade.

- Sectors are all in the green with Real Estate, Tech & Construction benefitting from yields while Travel & Leisure lifts after strong Lufthansa comments. Elsewhere, Delivery names benefit from the main takeaway of DoorDash's numbers.

- Stateside, futures reside in the green but with action slightly more contained than Europe as the region has already had a chance to react to the Fed, ES +0.4%; NQ +0.7% continues its outperformance amid ongoing yield action ahead of Apple earnings after-hours.

FX

- DXY continues to drift amidst peak Fed rate perceptions with the index towards the base of a 106.490-150 range.

- Antipodes extract most from their US rival's demise and buoyant risk appetite as Kiwi probes 0.5900 and Aussie approaches 0.6450.

- Euro, Franc and Yen all up at Dollar's expense, with EUR/USD back on a 1.0600 handle, USD/CHF straddling 0.9050 and USD/JPY closer to 150.00 than 151.00.

- Pound mixed awaiting BoE as Cable eyes 1.2200 and EUR/GBP rebounds through 0.8700.

- PBoC set USD/CNY mid-point at 7.1797 vs exp. 7.3055 (prev. 7.1778)

- Norwegian Key Policy Rate N/A 4.25% vs. Exp. 4.25% (Prev. 4.25%); "the policy rate will likely be raised in December". "If the Committee becomes more assured that underlying inflation is on the decline, the policy rate may be kept on hold”. Click here for more detail, reaction & analysis.

- Brazil Central Bank cut the Selic rate by 50bps to 12.25%, as expected, while committee members unanimously anticipate similar reductions in the next meetings. BCB added that this pace is appropriate to keep the necessary contractionary monetary policy for the disinflationary process and noted the external environment is adverse due to higher long-term interest rates in the US.

Fixed Income

- Bonds continue to bull-flatten as markets pre-empt policy pivots from tightening to easing.

- Bunds, Gilts and T-notes are all closer to peaks than troughs within 130.06-129.48, 94.35-93.44 and 107-13+/02+ respective ranges.

- OATs and Bonos firmly underpinned following well-received French and Spanish auctions.

Commodities

- Crude benchmarks are in the green with XAU and base metals also firmer in a continuation of post-Fed/Powell price action.

- WTI Dec’23 and Brent Jan’24 are posting gains of circa. USD 1.50/bbl on the session and reside around the USD 82.00/bbl and USD 86.00/bbl remarks. However, this remains well within Wednesday’s bounds and by extension some way shy of the USD 83.40/bbl and USD 87.00/bbl peaks for that session.

- Spot gold is benefitting from the aforementioned post-Powell trade as the USD and yields continue to slip. However, upside for the yellow metal is capped as the overall risk tone remains very constructive ahead of additional Tier 1.

- Base metals generally benefit from the risk tone with specifics light once again though Dalian Iron Ore continues to outpace in a move attributed to demand, low inventories and improved Chinese sentiment around stimulus.

Geopolitics: Israel-Hamas

- Lebanon's Hezbollah said it destroyed an Israeli drone with a surface-to-air missile in the airspace of two border villages, according to Reuters.

- Iran's Foreign Minister warned of 'harsh consequences' if an immediate ceasefire in Gaza doesn't take place and "rapid attacks by US and the Zionist Regime continue", according to Reuters.

Geopolitics: Other

- US military said a US destroyer and Canadian frigate transited through the Taiwan Strait yesterday, while the Chinese military said it followed the bilateral naval transit of the US and Canada in the Taiwan Strait, according to Reuters.

- China's Foreign Ministry says next week China and the US will hold director-general level consultations on arms control and non-proliferation, a delegation to be led by a senior official from the Foreign Ministry. In response to and confirmation of an earlier WSJ article

US Event Calendar

- 08:30: Oct. Initial Jobless Claims, est. 210,000, prior 210,000

- 08:30: Oct. Continuing Claims, est. 1.8m, prior 1.79m

- 08:30: 3Q Unit Labor Costs, est. 0.3%, prior 2.2%

- 08:30: 3Q Nonfarm Productivity, est. 4.3%, prior 3.5%

- 10:00: Sept. Factory Orders, est. 2.3%, prior 1.2%

- 10:00: Sept. Factory Orders Ex Trans, est. 0.8%, prior 1.4%

- 10:00: Sept. Durable Goods Orders, est. 4.7%, prior 4.7%

- 10:00: Sept. Durables-Less Transportation, est. 0.5%, prior 0.5%

- 10:00: Sept. Cap Goods Ship Nondef Ex Air, prior 0%

- 10:00: Sept. Cap Goods Orders Nondef Ex Air, est. 0.6%, prior 0.6%

DB's Jim Reid concludes the overnight wrap

I woke up this morning to my garden looking like a battleground as I made my regular pre-EMR strong coffee. Debris lays all around from storm Ciaran. Thankfully the trampoline looks like it held the line. As southern England mops up from the storm, the FOMC helped clear up a lot of the debris from recent weakness in both bonds and equities yesterday.

Indeed it was the best day for US Treasuries since March (10yr yield down -19.7bps) as a dovish leaning FOMC outcome reinforced an already strong rally driven by the Treasury’s refunding announcement and weaker US data. A softening of the Fed’s tightening bias and the bond rally supported equities, with the S&P 500 (+1.05% yesterday) seeing its strongest three-day rally since late March. I wonder whether the seasonals are also kicking in. As we showed in our CoTD last Friday (link here), that day (October 27th) is on average the low point for the S&P between July and October. After that markets on average rally. The next big events are the BoE today and Apple earnings after the closing bell tonight before payrolls tomorrow .

Starting with the Fed, as widely expected the FOMC held rates steady and the prepared statement largely saw a holding pattern, with one notable change being a new mention of tighter financial conditions. This dovish tilt was again visible in Powell’s prepared remarks, with a more direct comment that “the stance of policy is restrictive”. In the Q&A, Powell maintained a tightening bias, repeating the message that strong growth could warrant “further tightening’ and saying that the FOMC were ”not confident yet” that they have achieved a “sufficiently restrictive stance”. So keeping the possibility of a hike in December on the table, while also dismissing the idea that it would be “difficult to raise again after stopping for a meeting or two”.

However, Powell’s overall tone made this tightening bias sound rather soft, with several less hawkish elements. T here was repeated focus on the tightening in financial conditions, although this “would need to be persistent” for it to matter for policy. And while Powell said that “likely we will need to see some slower growth and softening in the labour market conditions”, he highlighted how positive supply effects (labour participation, immigration, supply chains) have helped bring inflation down so far. Powell echoed some of his recent comments with a dovish-leaning take on the labour market, noting the slowing of wage growth and saying that the recent ECI release was very close to Fed expectations. Finally, Powell acknowledged that “the risk of doing too much versus the risk of doing too little are getting closer to balance“. Away from rates policy, a notable comment was that the FOMC “is not considering” changing the pace of QT and that “it’s hard to make a case that reserves are even close to scarce at this point" .

Our US economists continue to expect that the Fed is done raising rates, but with this requiring evidence of a moderation in growth and labour market data as well as financial conditions remaining tight or tightening further. See their full reaction note here. Indeed, with Powell seeing persistence of tighter financial conditions as “critical”, we can’t help but wonder whether yesterday’s dovish market reaction could incentivise some hawkish pushback, especially if it continued.

Rates markets took firm hold of the Fed’s dovish hints, with futures now pricing a 19% chance of hike at the December meeting (down from 27% the previous day), and Dec-24 pricing falling by a sizeable -17.9bps to 4.49%. This repricing saw 2yr Treasury yields fall by -14.3bps to 4.95%, with just over half of the decline coming post the FOMC decision. And 1 0yr yields saw their sharpest rally since the March banking stress, down -19.7bps to 4.73% (though they were already down by -13bps prior to the Fed). The entirety of the move came from real yields, with the 10yr down -20.0bps. Overnight, 10yr yields (-1.68bps) are dipping further, with the 2s10s curve flattening (-2.92bps) and standing at -24.1bps as we go to print, thus doubling the level of inversion in a couple of days.

Equities saw some volatility during Powell’s comments, but the risk-on takeaway dominated with the S&P 500 closing up +1.05%, having traded c.+0.4% higher prior to the FOMC decision. T his brings the gains so far this week to +2.93%, which as mentioned at the start is its strongest rally since late March. Tech stocks led the advance with the NASDAQ up +1.64% and the Magnificent Seven mega cap index up +2.68% .

Ahead of the Fed, the main story driving markets was the Treasury refunding announcement, which triggered a major rally for Treasuries. That was because they only announced sales of $112bn of longer-term securities (vs. $114bn expected), and the increase in the issuance of 10yr and 30yr Treasuries was smaller than the increases in August. In the statement from the Treasury, they said they anticipated that “one additional quarter of increases to coupon auction sizes will likely be needed beyond the increases announced today .” With regard to buybacks, they said that “ Treasury continues to make significant progress on its plans to implement a regular buyback program in 2024 .” And looking forward, it said there’d be an update on timing in the next quarterly refunding announcement. See Steven Zeng’s review of the event here. Although it ended up in line with his lower than consensus expectations, he sees it as a major positive development for the Treasury market.

The bond rally after the announcement was cemented by another round of weak data releases. In particular, the latest US ISM manufacturing release fell to 46.7 in October (vs. 49.0 expected), which ended a run of three consecutive gains, whilst the new orders subcomponent also fell to a 5-month low of 45.5 (vs. 49.8 expected). That mood wasn’t helped by another weak ADP report, which signalled that private payrolls were only up +113k in October (vs. +150k expected), and the 3-month rolling average (+127k) fell to its lowest since March 2021. Moreover, we had the MBA’s latest weekly index of mortgage applications, which fell to another post-1995 low over the week ending October 27 .

The one release which didn’t fit into this trend was the latest JOLTS report for September, which showed a tighter labour market than expected. For instance, job openings were up to a 4-month high of 9.553m (vs. 9.4m expected), which meant that the ratio of job openings per unemployed individuals was still above its pre-pandemic levels at 1.50. In the meantime, the quits rate of those voluntarily leaving their jobs held steady at 2.3%, in line with pre-pandemic levels. Overall, while the US labour market is no longer extraordinarily tight, the latest data suggest its normalisation could be slowing.

Looking forward, central banks will remain in the spotlight today, as the Bank of England announce their latest decision on rates. Like the Fed, they’re widely expected to keep rates on hold, having already paused their hikes at the last meeting in September. So the main focus will instead be on how the vote breaks down and the BoE’s new forecasts. In his preview (link here), our economist expects a 6-3 vote count to keep rates on hold, with the 3 voting in favour of another 25bp hike. With regards to the forward guidance, he expects no changes, and sees the MPC reiterating its view that policy will remain sufficiently restrictive for sufficiently long to get CPI sustainable back to 2%.

Before all that, European markets put in another solid performance, and the STOXX 600 (+0.67%) posted a 3rd consecutive advance. Sovereign bonds also did well, with yields on 10yr bunds (-4.3bps), OATs (-4.6bps) and BTPs (-5.8bps) all falling back, although UK gilts (-1.4bps) were a slight underperformer ahead of the BoE decision today.

Asian equity markets are joining in the global rally with the KOSPI (+1.77%) outperforming followed by the Hang Seng (+1.21%), the Nikkei (+1.01%), the Shanghai Composite (+0.11%) and the CSI (+0.10%). S&P 500 (+0.26%) and NASDAQ 100 (+0.43%) futures are ticking higher.

Early morning data showed that South Korea’s inflation accelerated to a seven-month high of +3.8% y/y in October (v/s +3.6% expected and 3.7% last month), due to higher prices of energy and farm goods. This will make it more likely that the Bank of Korea (BOK) keeps its restrictive stance in place for longer. Elsewhere, Australia’s trade surplus narrowed more than expected to A$6.78 billion from A$10.16 billion in September with exports falling -1.4% m/m, reversing the prior month’s revised advance of +4.6% while imports strongly rebounded +7.5% m/m after a -0.8% drop in the prior month.

Moving to Japan, Prime Minister Fumio Kishida announced a stimulus package worth more than $100 billion (higher than consensus expectations) as the incumbent PM is facing higher inflation while at the same time grappling with his poll ratings being at a record low since taking office in 2021. The package’s highlight is income and residential tax rebates to low-income households. Following the BOJ’s yesterday announcement of an emergency bond-purchase operation, plus the global rally, y ields on 10yr JGBs have come down to 0.92% after touching a high of 0.97% yesterday a level last seen in May 2013 .

To the day ahead now, and one of the main highlights will be the Bank of England’s latest policy decision and the subsequent press conference where we’ll hear from Governor Bailey. Otherwise, central bank speakers include the ECB’s Lane and Schnabel. Data releases from the US include the weekly initial jobless claims and September’s factory orders, whilst there’s also German unemployment for October. Finally, today’s earnings releases include Apple and Starbucks.