In a clear sign we are reverting to a system where fiscal policy dominates monetary policy, the Treasury’s refunding announcement is probably more consequential than the Federal Reserve’s meeting today. An increased skew away from bill issuance is a headwind for liquidity and risk assets.

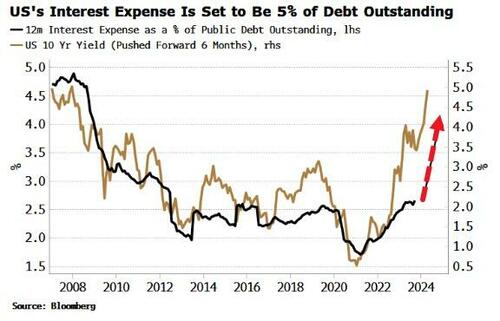

The refunding announcement is in focus due to the US’s huge fiscal deficit. It comes when rising yields – i.e. loose fiscal policy meets tight monetary policy – means the government’s interest-rate costs are soaring.

The rapid rise in US yields to ~5% points to the government’s annual interest-rate bill rising to 4.5-5% of debt outstanding in the next six months. That’s in the region of $1.7 trillion - or the GDP of Australia - each year.

Such large payments are negative for the economy. Interest is likely to be paid for using higher-velocity money (e.g. taxes) and received by holders less likely to spend the proceeds in the broad economy, and instead re-invest it. Independent monetary policy becomes increasingly difficult when the equivalent of 6% of US GDP is being diverted towards interest payments each year.

It’s not only the size of Treasury borrowing that’s a problem, but it’s maturity composition.

Issuance has latterly been skewed to bills, which has ameliorated the impact on liquidity as money market funds have been able to intermediate through the reverse repo (RRP) facility at the Fed. But as issuance skews back towards longer-term debt (watch for increases in auction sizes in 2y, 3y, 5y, 7y, 10y, 20y and 30y debt for insight on this), that will have an increasingly negative impact on liquidity, especially if the Treasury maintains its large cash balance at the Fed (as it said on Monday it expected to do).

The Fed has little (or no) say over any of this.

Monetary policy will become increasingly overwhelmed in such an environment, which is why today’s Fed meeting, where it is expected to keep rates on hold, is a bit of an afterthought.

Also of more consequence currently is Japan.

The BOJ’s decision to maintain negative yields and keep its yield curve control policy largely intact ladles on yet more underlying risks to the global macro environment.