With a stunning trillion dollars added to the national debt in only three months, projected to reach an incomprehensible $54 trillion within 10 years, and America’s interest payments on track to exceed defense spending next year, the question must be asked: How much longer can the debt bubble go?

It’s a curious situation when Jerome Powell, a man who oversaw the largest money-printing campaign in American history, is saying that the debt is unsustainable. While maintaining that the Fed “tries hard not to comment on fiscal policy,” Powell’s suggestion for handling the debt shifts blame and burden from money printing to fiscal irresponsibility on the part of policymakers.

While they have their part to play, and it’s a big one, it’s interesting to see that Federal Reserve monetary policy hasn’t been mentioned in any of Powell’s ‘urgent’ warnings about ballooning debt:

“In the long run, the U.S. is on an unsustainable fiscal path. The U.S. federal government’s on an unsustainable fiscal path. And that just means that the debt is growing faster than the economy. So, it is unsustainable. I don’t think that’s at all controversial. And I think we know that we have to get back on a sustainable fiscal path.”

It’s a wonder how, even if the government suddenly adopted responsible spending and budgeting, we would be back on a path of true sustainability after Powell oversaw the printing of over 3 trillion dollars in 2020 alone. The Fed is an interesting source of criticism for unsustainable debt, to say the least:

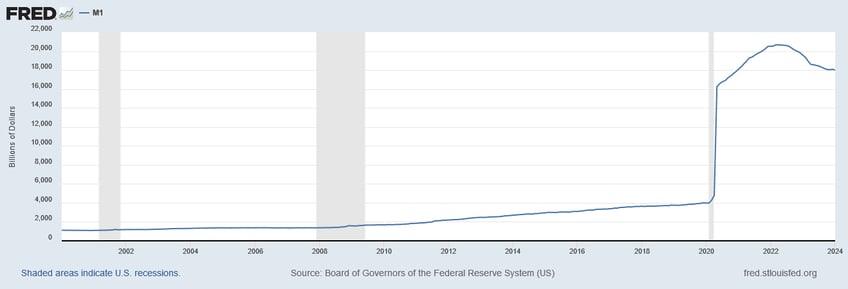

M1 Supply Growth (Billions), 2000-2024, From St. Louis Fed Data

Source: Board of Governors of the Federal Reserve System (US), M1 [M1SL], retrieved from FRED, Federal Reserve Bank of St. Louis; March 6, 2024.

But as usual, the Fed only has one real tool in its toolbox: tinkering with interest rates directly to stimulate or disincentivize borrowing, or indirectly by firing up the money printer. Rate cuts expected later this year will reduce the burden of interest payments on debt growth, but simultaneously will flood the economy with newly-created money. People, already over-indebted and using credit cards for basic needs, will take advantage of a lower cost of borrowing and sign up for more loans for expenses and goods that they can’t really afford.

More loans and more deposits will increase M1 in an already-frothy inflationary environment, adding pressure to a pot that’s already in danger of boiling over from money printing during Covid. Post-COVID rate hikes have not even come close to reversing this course, with interest still far lower than it would be in an actual free market, where a few dozen bureaucrats would no longer be pulling the levers. Excessive borrowing makes US Treasurys less...(READ THIS FULL ARTICLE, FREE, HERE).