Background: This year’s second BOA RIC report covers how to position for what the Bank believes are the most likely scenarios in 2024; Specifically a soft landing followed by inflation reignition

Contents:

Intro: From Soft Landing to Inflation Reignition

Buy Real assets for an inflation rebound

Gold- (GLDM)

Regional Oil- (KSA)

Uranium- (URA)

Mining Shares (XME)

Why (The Fed) Can’t Touch This Inflation

Data says inflation is not dead at all

Government spending

Households have money to spend

Wages are high and not coming down

Footnotes, More

1- From Soft Landing to Inflation Reignition

At the top of it, the RIC Outlook expects slower growth and inflation in most of the world next year at first. Central banks will likely respond by cutting rates (at least 4 times according to Goldman) and most economies will thus avoid recession, supporting markets.

This implies soft landings and inflation reignitions in combination as their most likely scenario. Half of the report is concerned with what assets will benefit most from a soft landing. The other half is focused on two things:

What will benefit post the expected inflation reignition.

What the Fed has no control over inflation-wise

That is our focus here. From the report’s summary

We think that Fed cuts next year could reignite structural inflationary forces. Consider the parts of the economy proving robust, even impervious, to rate hikes: record government deficits; high household savings, rising wages & record home prices; corporates cushioned by private credit and cash.

These metrics in Exhibit 1 are 1-2 standard deviations above long-term norms. There seems to be a lack of slack.

And here is how they suggest investors position for that eventuality.

2- Buy Real assets for an inflation rebound

Excerpted from BOA’s 2024 Research Investment Committee Report1

Structurally higher rates and inflation suggest the returns and correlations of major asset classes over the past two decades is an anomaly.

[EDIT: That is a powerful statement synopsizing Hartnett’s big picture opinion. Restated: We are in a new world of structural inflationary headwinds making normal financial correlations untrustworthy as said in this space before.]

Inflation is still an upside risk. Balancing portfolios with gold and resource equities can help improve resilience.

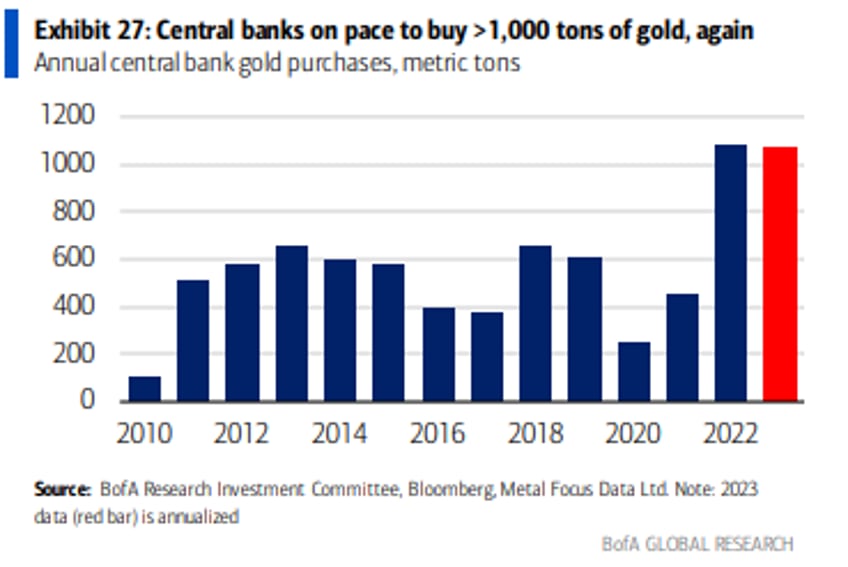

Gold (GLDM) gold is the consummate inflation and risk-off hedge for long-term investors. Central banks are on pace to buy >1000 tons of gold for the second year in a row which has helped bolster gold prices despite higher real rates (Exhibit 27).

Also note: they advise one hedges inflation risk, but not assuming rampant inflation … although in another report they are concerned for the Fed having to un-pivot and actually raise rates.

The last time US 10-year real yields were above 2%, gold traded between $700-800/oz and lower yields next year could bolster gains. Michael Widmer expects gold prices to be flat but sees scope for $2,400 in a risk-off scenario.

Saudi Arabia (KSA) is KSA is a strong oil proxy, provides access to strong Saudi balance sheets, and is a good hedge if escalation of the Middle East conflict pushes oil to $130/bbl. Our economists are bullish on Saudi Arabia’s economy outside of energy and think a strong fiscal impulse supports a robust growth outlook.