Tuesday's post-hot CPI dump now seems like a distant bad dream as US equity futures continued their rebound, following a tech fueled rally on Wednesday that drove the S&P 500 back above 5,000. As of 8:05am, S&P 500 futures were up 0.1%, also approaching pre-CPI levels; Nasdaq futures were as usual even stronger, rising 0.2% Europe’s Stoxx 600 index surged to the highest in more than a month. WTI crude oil futures are down 0.8% on heels of 1.6% drop Wednesday, following a bearish report by the IEA which predicts lower demand growth than supply growth in 2024. Today’s macro focus is on Retail Sales and Jobless data amid the barrage of data which includes import/export price indexes, Empire State manufacturing and Philadelphia Fed business outlook surveys, January industrial production, December business inventories, February NAHB housing market index and December TIC flows. A weaker print in retail sales - which our preview suggested is coming - and claims may continue the rally in bonds, potentially pushing the Equity rotation that began last week (paused with CPI) farther. There are also three Fedspeakers today.

In premarket trading, Cisco fell 4% after the maker of computer networking equipment slashed its full-year forecast, and announced it would lay off 5% of its workforce, prompting more questions about this chimeric earnings renaissance thanks to AI which has yet to come. Here are some other notable premarket movers:

- Albemarle falls 4% after the lithium producer gave pricing guidance that disappointed Wall Street.

- AppLovin jumps 22% after the mobile app marketing platform reported robust fourth-quarter earnings.

- Fastly falls 21% after the infrastructure software company gave a revenue forecast that was weaker than expected.

- JFrog jumps 18% after the software development company reported fourth-quarter results that beat expectations.

- Manchester United falls 15% as the Friday deadline for billionaire Jim Ratcliffe’s tender offer nears.

- Nu Skin plummets 24% after the beauty and wellness company failed to meet first-quarter revenue guidance expectations and cut its quarterly dividend.

- Paramount Global slips 4% after a filing from Berkshire Hathaway showed the firm had reduced its stake in the media company.

- SoundHound AI soars 84% after Nvidia filed a 13F indicating that it holds a stake in the company. The chipmaker also disclosed a stake in Nano-X Imaging and Recursion Pharmaceuticals.

- Nano-X Imaging +56%, Recursion Pharmaceuticals (RXRX) +21%

- Twilio slides 11% after the software company issued first-quarter revenue guidance that was slightly weaker than anticipated.

- Yeti declines 12% after its adjusted earnings per share forecast for the year missed the average analyst estimate.

Wednesday’s powerful rebound, fueled by a wave of dip buyers, showed that investors should avoid making hasty conclusions on the back of a single data point, according to Julian Emanuel, chief equity strategist at Evercore ISI.

“The clear implication of what we’ve seen in the last few days is don’t trade the numbers,” Emanuel said in an interview with Bloomberg TV. “If you traded CPI after the number, you’re already far underwater given the bounceback we had yesterday. Thinking about the last 40 years you make money by buying pullbacks.”

To be sure, mostly favorable earnings reports have been a boon for investors hammered by Tuesday’s hotter-than-expected US inflation reading and disappointed they may have to wait longer for interest rate cuts. Treasuries also rebounded as investors braced for more economic reports that could help determine the Federal Reserve’s rate path. Data due later include initial jobless claims, industrial production and retail sales which BofA's card spending data suggests will be a big miss to expectations.

“The ‘hot’ inflation data do not change our base case for a soft landing,” said Solita Marcelli at UBS Global Wealth Management. “But we are continuing to monitor the incoming data and the start of rate cuts could be delayed should the economic prints remain strong.”

European stocks rose for a second day, with the Stoxx trading at session highs up 0.9%, although the FTSE 100 has struggled to keep pace after the UK slipped into a mild recession in the second half of 2023. European bourses were sharply higher, with autos leading the gains, buoyed by Stellantis’ buyback announcement, while energy stocks are the biggest laggards. Here are the biggest European movers:

- Stellantis shares rise as much as 4.9%. Bernstein says the carmaker’s planned €3 billion share buyback program and its higher dividend are “encouraging.”

- Pernod Ricard shares rise as much as 6.3% after the cognac maker’s 1H recurring operating income met estimates, while it posted a lower-than expected decline in organic growth.

- DSM-Firmenich shares rise as much as 15% after the specialty chemicals company announced plans to separate its Animal Nutrition & Health and posted a 4Q Ebitda beat.

- Legrand shares gain as much as 4.4% after the French electrical devices manufacturer posted another solid set of results, with free cash flow as the highlight, according to Morgan Stanley.

- Genmab shares surge as much as 12%, the most intraday since March 2020, after the Danish biotech firm reported results and said it will repurchase up to 190,000 shares.

- Renault shares rise as much as 5.1% after the French car company generated far more cash than expected, allowing it to bolster its balance sheet and hike its dividend.

- Centrica shares gain 6.1% after the UK utility reported results which analysts said were boosted by strength in the commodity-exposed Energy division, although otherwise in line.

- Tomra shares surge as much as 26%, the most since Dec. 1993, following a “solid” fourth-quarter beat by the Norwegian recycling systems maker.

- Kerry Group shares fall as much as 6.1%, the most in almost two years, after the ingredients company missed expectations in 2023 and issued disappointing guidance for the year ahead.

- Gecina shares fall as much as 5.5% following results that saw an acceleration in the decline of property valuations.

- Verallia shares drop as much as 3% after fourth-quarter results that Citi says missed expectations, as continued destocking offset pricing increases by the glass bottle manufacturer.

- Embracer shares slump as much as 14% after the video-game company said it’s unlikely to reach its net debt reduction target by end of March.

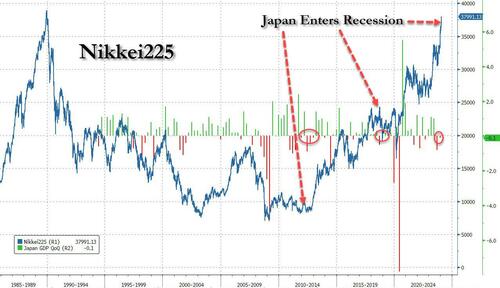

Earlier in the session, Asian stocks rose with Japan stocks shaking off worse-than-expected GDP numbers and Hong Kong overcomes early declines. The Aussie slips and bonds rise after a lower-than-forecast jobs number. Hong Kong’s tech gauge leads the city’s gainers, rising 0.6%. In Japan, the Nikkei adds 1% and is rapidly approaching its all time high set in 1989 even as a recession strikes...

... while the Topix underperforms, climbing 0.2%. Indonesia’s stocks rise as Prabowo Subianto looks poised to win the nation’s election. In currencies, the Aussie dips to the day’s low of 64.78 US cents while the yen rises slightly, adding 0.2% after the nation’s GDP contracted versus an expected gain. JGBs rise.

In FX, the Bloomberg dollar index dropped, while the concurrent slide of two major G-10 countries in recession had opposite effects on their currencies: Japan's yen shrank while the pound slumped, and was the weakest G-10 currency, falling 0.1% versus the greenback. The yen climbed for a second day, paring some of the US CPI-induced weakness earlier this week that spurred verbal warnings from Japanese authorities. The Aussie steadied following an earlier dip driven by soft jobs data, which brought forward RBA rate cut bets. The yen fluctuated earlier after data showed Japan’s gross domestic product contracted at an annualized pace of 0.4% in the final three months of last year, shrinking for a second quarter and prompting some BOJ watchers to push back bets on when the negative interest rate policy will end

“With verbal interventions from the authorities, concerns about the real action prevail in the market, making it hard for market players to test the dollar-yen’s upside,” said Tsutomu Soma, a bond and currency trader at Monex Inc. “However, the downside is also limited to some extent because even if the BOJ scraps negative rate policy, wide yield gap still remains as it will be very cautious to lift the rate from zero.”

In rates, treasuries rise as investors look ahead to a busy US data calendar that includes retail sales and industrial production. Gains for Treasury futures during Asia session and European morning trim yields by 2bp to 4bp across the curve and leave 2s10s, 5s30s spreads slightly flatter on the day, as the surge in yields sparked by January CPI data Tuesday drew dip-buyers and continues to be unwound. 10-year TSY yields are around 4.225% is ~3bp richer on the day, outperforming bunds and gilts in the sector by ~1bp; front-end Treasuries lag slightly, flattening 2s10s, 5s30s spreads by 1bp and 0.5bp on the day, partially unwinding Wednesday’s steepening move. US session features a heavy economic data calendar including retail sales, weekly jobless claims and industrial production.

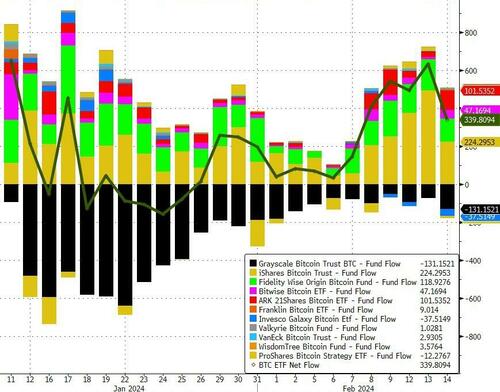

In commodities, oil prices decline, with WTI falling 0.7% to trade near $76.10. Spot gold adds 0.2%. Bitcoin rises ~1% to trade above $52,000.

Bitcoin (+0.9%), continues its advances, but has so far found resistance around the $52.5k level. Ethereum currently just shy of USD 2.8k. Bitcoin ETF inflows continued apace if modestly off yesterday's record high.

Finally looking to the day ahead, in terms of US data we get January retail sales and import/export price indexes, February Empire State manufacturing and Philadelphia Fed business outlook surveys and weekly jobless claims data (8:30am), January industrial production (9:15am), December business inventories, February NAHB housing market index (10am) and December TIC flows (4pm). Elsewhere, we got UK Q4 GDP (which unexpectedly joined Japan in sliding into recession), Eurozone December trade balance, Canada January housing sales and December manufacturing sales. We will be hearing from the ECB’s Lane and Nagel, and the BoE’s Greene and Mann. Finally, earning releases include Applied Materials, Deere, Stellantis, DoorDash, DraftKings, and Roku.

Market Snapshot

- S&P 500 futures up 0.1% to 5,025.00

- STOXX Europe 600 up 0.5% to 487.85

- MXAP up 0.9% to 169.07

- MXAPJ up 1.0% to 516.53

- Nikkei up 1.2% to 38,157.94

- Topix up 0.3% to 2,591.85

- Hang Seng Index up 0.4% to 15,944.63

- Shanghai Composite up 1.3% to 2,865.90

- Sensex up 0.3% to 72,033.24

- Australia S&P/ASX 200 up 0.8% to 7,605.72

- Kospi down 0.3% to 2,613.80

- German 10Y yield little changed at 2.32%

- Euro little changed at $1.0735

- Brent Futures little changed at $81.55/bbl

- Brent Futures little changed at $81.53/bbl

- Gold spot up 0.1% to $1,994.80

- U.S. Dollar Index down 0.10% to 104.62

Top Overnight News

- Japan’s Q4 GDP falls short as the country unexpectedly slips into recession (GDP in Q4 came in -0.4% vs. the Street +1.1%). RTRS

- TSMC surged the most in more than three years on AI prospects, propelling Taiwan’s benchmark index to a record. BBG

- While most containerships are making detours around the conflict-affected Red Sea, experts say container freight rates, which had initially soared, are showing signs of easing. "We believe that the worst is behind us," said Philip Damas, managing director at British maritime research consultancy Drewry. "Now we are into a second phase where it will be easier for exporters to manage and organize, and also where the spot rates are going to come down significantly after the early phase." Nikkei

- ECB’s Lagarde says inflation is moving in the right direction, but the central bank requires additional data before implementing rate cuts. RTRS

- UK economy falls into recession in 2nd half of 2023, with Q4 GDP undershooting expectations (-0.3% vs. the Street -0.1%) although the Dec numbers (GDP, industrial production, and manufacturing production) came in above plan. RTRS

- The looming Israeli military plans to invade Rafah have exacerbated tensions between Israeli Prime Minister Benjamin Netanyahu’s government and the Biden administration, which has grown increasingly frustrated with its attempts to rein in Israel’s military campaign. WSJ

- Israel on Wednesday launched its longest and heaviest attack on neighboring Lebanon since the start of the Gaza war, striking several locations in the south, killing at least three Hezbollah fighter and seven civilians, and raising further the specter of war between the two long-standing enemies. WaPo

- Deere (-4% premkt) downgraded its annual profit outlook as falling crop prices lower demand for equipment. Cisco also fell 4% premarket after slashing its full-year forecast and announcing plans to cut about 5% of its workforce. BBG

- Crude will potentially be in surplus this year as demand growth loses steam and supplies from outside OPEC+ continue to swell, the IEA said. The agency stuck to its 2024 demand growth forecast of 1.2 million barrels a day while forecasting non-OPEC+ supplies to rise by 1.6 million b/d, led by the US and Brazil. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly took impetus from the rebound on Wall St after the Fed downplayed the recent CPI report. ASX 200 was led higher by a rally in tech and real estate but with upside capped by disappointing jobs data. Nikkei 225 climbed back above the 38,000 level and printed a fresh 34-year high with the index largely unfazed by the surprise contraction in Q4 GDP which showed that Japan's economy entered into a technical recession. Hang Seng traded rangebound amid quiet newsflow and the continued absence of mainland participants

Top Asian News

- Japan's Cabinet Office said 2023 nominal GDP undershoots Germany's to become the world's fourth largest economy in dollar-denominated terms and that weak domestic demand for clothing and eating out caused a decline in private consumption.

- Japan's Economy Minister Shindo said consumer spending lacks strength and capex is taking time to realise, while he added the government aims to achieve wage increases that surpass inflation, leading to consumption growth. The government also aims to boost the potential growth rate by promoting domestic investment and aims to realise a virtuous cycle of wage increase and economic growth.

- Monetary Authority of Singapore official said monetary policy is appropriate and the next policy statement is scheduled for April. MAS also noted there are continuing uncertainties on growth and inflation which it is monitoring the implications of quite closely.

- RBA Governor Bullock said the global economy held up better than initially expected and had been worried about hard landings and recessions, while she added they are in a good position to get inflation down in a reasonable amount of time.

- Japanese Chief Cabinet Secretary, when asked about GDP, says they will mobilise all available policies to achieve higher growth and wage increases that exceed inflation

European bourses, Stoxx600 (+0.5%) began the session entirely in the green and continued to extend throughout the European morning. The CAC 40 (+0.9%) incrementally outperforms after a slew of strong results from heavyweight names within the index. European sectors hold a positive tilt with Autos parked at the top of the pile, assisted by gains in Renault (+5.5%), with Industrials also benefitting from post-earning strength in Safran (+3.6%) and Schneider Electric (+3.2%). US Equity Futures (ES +0.1%, NQ +0.1%, RTY +0.9%) are modestly firmer, though with clear outperformance in the RTY, as it continues the prior day's outperformance. Cisco (-5.5%) reported generally strong metrics, though did provide soft guidance. Goldman Sachs on European Stocks: raises 12-month Stoxx 600 target to 510 (prev. 500; last close 485). upgrade Travel & Leisure to Overweight from Neutral; upgrade Consumer Products & Services to Overweight from Neutral; downgrade Energy to Neutral from Overweight; downgrade Utilities to Underweight from Neutral.

Top European News

- Goldman Sachs cuts the UK's 2024 GDP growth forecast to 0.4% (prev. 0.6%)

- ECB President Lagarde says "the latest data confirm the ongoing disinflation process and is expected to bring us gradually further down over 2024 as the impact of past upward shocks fades and tight financing conditions help to push down inflation". New framework will most likely compromise bond portfolio and lending operations; we will be done with framework review in a couple months. "Last thing I want is hasty decision and then inflation rises again".

- ECB's de Cos says bank's projections foresee inflation to continue falling; still need some time on the exact timing of rate cut

- Germany's DIHK: German Co's expect economy to shrink in 2024 and GDP to contract by 0.5%; 35% of surveyed Co's expect business to worsen in next 12m, 14% expect improvements. Bad sentiment in German economy is rising. Expects inflation of 2.7% exports to grow by 0.5%, private consumption spending to grow by 0.5% in 2024. 57% of Co's see economic policy framework in Germany as business risk. 33% of German Co's plan to decrease investments in Germany, 24% plan investment expansions.

- Maersk (MAERSB DC) says as security risks remain highly elevated, vessels previously bound to transit area continue to be diverted south via Cape of Good Hope.

Earnings

- Cisco Systems Inc (CSCO) - Q2 2024 (USD): Adj. EPS 0.87 (exp. 0.84), Revenue 12.8bln (exp. 12.71bln); to cut about 5% of global workforce. KEY METRICS: Networking revenue 7.08bln (exp. 7.16bln). Security revenue 973mln (exp. 956.8mln). Collaboration revenue 989mln (exp. 966mln). Adj. gross margin 66.7% (exp. 65.7%). Adj. operating margin 33% (exp. 32.1%). FY24 GUIDANCE: Revenue 51.5-52.5bln (prev. 53.8-55.0bln, exp. 54.33bln). Adj. EPS 3.68-3.74 (prev. 3.87-3.93, exp. 3.87). Q3 GUIDANCE: Revenue 12.1-12.3bln (exp. 13.1bln). Adj. EPS 0.84-0.86 (exp. 0.92). Adj. gross margin 66-67% (exp. 65.8%). Adj. operating margin 33.5-34.5% (exp. 33.8%). Shares -5.5% in pre-market trade

- Airbus (AIR FP) - Q4 (EUR): Adj. EBIT 2.21bln (exp. 2.26bln). Revenue 22.9bln (exp. 22.5bln), sees 2024 deliveries about 800 planes (exp. 826). Co. is to propose a special dividend of EUR 1/shr. Sees 2024 adj. EBIT between 6.5-7bln (exp. 7.15bln). On widebody aircraft, the Co. continues towards a monthly rate of 4 aircraft for the A330 in 2024 and rate 10 in 2026 for the A350. Co. assumes no additional disruptions to the world economy, air traffic, the supply chain, the Company’s internal operations, and its ability to deliver products and services. (Airbus) Index Weightings: CAC 40 (4.8%), Euro Stoxx 50 (2.6%), Stoxx 600 (0.8%). Shares -1% in European trade

- Pernod Ricard (RI FP) - H1 (EUR): Sales 6.59bln (exp. 6.58bln), Net 1.57bln (exp. 1.43bln), Operating Profit 2.14bln (prev. 2.42bln), FCF 301mln. FY24 Outlook: Broadly stable net sales in H2 vs H1. EUR 300mln buyback for the year, EUR 150mln completed in H1. (Newswires) Shares +3.8% in European trade

- Renault (RNO FP) - FY23 (EUR): Net 2.32bln (exp. 3.52bln), Revenue 52.38bln (exp. 52.88bln). Proposes 1.85 dividend (exp. 1.37). FY24 Operating Margin view of "at least" 7.5%, FY24 FCF view "at least" 2.5bln. (Newswires) Shares +7.5% in European trade

- Schneider Electric (SU FP) - FY23 (EUR): adj. EBITA 6.41 (exp. 6.03bln, prev. 6.02bln Y/Y), Revenue 34.2bln (exp. 36.04bln, prev. 35.9bln Y/Y). Guides initial FY24 adj. EBITA organic +8-12%, organic sales +6-8%, Adj. EBITA margin +40-60%. CFO does not expect to implement big increases this year. (Newswires)

- Safran (SAF FP) - FY23 (EUR): Adj. Revenue 23.2bln (exp. 23.3bln), Op. 3.17bln (prev. 2.41bln Y/Y), Op margin 13.6% (exp. 13.8%). Guides initial FY24 adj. recurring op. close to 4bln, adj. revenue 27.4bln (exp. 26.69bln), FCF 3bln. Expects M&A activity to accelerate. (Newswires) Shares +2.5% in European trade

- Stellantis (STLAM IM/STLAP FP) - H2 (EUR): Net Revenue 91.176bln (exp. 91.1bln). Adj. Operating Income 10.217bln (exp. 9.54bln; -10% Y/Y). Adj. Operating Margin 11.2% (prev. 14.4% in H1). Co. plans a EUR 3bln open market share buyback program this year. OTHER METRICS: Dividend proposed of EUR 1.55 per common share, increase of approximately 16% compared to prior year, pending shareholder approval. Industrial free cash flows of EUR 12.9bln; +19% Y/Y. LEV sales up 27% in 2023, with PHEVs at 1 in U.S. and #2 for LEVs in US 21% increase in global BEV sales in 2023. OUTLOOK The Company is reiterating a minimum commitment of double-digit adjusted operating income (AOI) margin in 2024. Shares +4.5% in European trade

FX

- USD is steady ahead of a deluge of US data. For now, a test of 105.00 in the index is yet to materialise after yesterday's 104.97 peak. If 105.00 goes, there is clean air until 105.73 which was the November 14th peak.

- EUR has picked up from yesterday's 1.0695 YTD trough in light of EZ-specific newsflow, and unreactive to ECB Lagarde. Upside sees the 10DMA at 1.0755 and 100DMA at 1.0794 ahead of the 1.08 mark.

- GBP is softer vs. the USD as GDP data sees the UK enter into a technical recession. Cable printed a low of 1.2543 but stopped short of yesterday's 1.2536 trough.

- JPY is firmer vs. the USD despite soft Japanese GDP metrics. Pullback could be a combination of technical factors after the pair ran out of steam at 150.88 as well as increased jawboning from Japanese officials.

- AUD a touch firmer vs. the USD despite disappointing jobs data overnight. AUD/USD has made a high of 0.6501 but is yet to materially clear the level or test the pre-US CPI peak of 0.6537.

Fixed Income

- Gilts are firmer after the regions GDP print sparked a dovish gap-up of 49 ticks to a 98.29 open before extending to a 98.59 peak. Overall, the data was dovish but is unlikely to have any significant impact on the BoE's calculus for the first cut.

- USTs are in-fitting with price action seen in Gilts/Bunds; specifics light into a busy afternoon agenda; usual weekly data and Fed's Waller the highlights. As it stands, USTs at the top-end of 110-00+ to 110-10 bounds while the yield curve is slightly flatter.

- Bunds are firmer in tandem with Gilts. Currently up to 134.18 at best, but have since retreated back beneath 134.00 as newsflow slows with Chief Economist Lane the afternoon highlight.

- Spain sells EUR 5.896bln vs exp. EUR 5-6bln 2.50% 2027, 3.50% 2029 and 2.35% 2033 Bono

- France sells EUR 11.992bln vs exp. EUR 10.5-12bln 2.50% 2027, 2.75% 2029 and 0.00% 2031 OAT

Commodities

- Crude is subdued following the large inventory builds in the prior session. Markets are seemingly putting more weight on the demand implications of recession as opposed to the supply concerns from expanding geopolitics. Currently, Brent holds just above USD 81.00/bbl.

- Upward biases across precious metals following the recent pullback in the Dollar, yields and amidst the heightened geopolitical landscape; XAU found intraday support close to its 100 DMA (1,990.35/oz).

- Base metals are mostly firmer albeit with mild gains amid the slight pullback in the Dollar after Fed officials downplayed the recent hot US CPI report.

- IEA OMR: 2024 global oil demand growth downgraded by 200k BPD to 1.22mln BPD (prev. 1.24mln); says global oil demand growth is losing momentum, with pace of expansion set to decelerate from 2.3mln BPD last year, in part due to China. With the robust outlook for non-OPEC+ supply, our balances suggest a slight build in inventories in 1Q24 despite the extension and deepening of OPEC+ supply curbs. From 2Q24 onwards, continuation of this strength could leave OPEC+ pumping above requirements for its crude oil if extra voluntary cuts are unwound in the second quarter.

- Iran sets the March Iranian light crude OSP to Asia at Oman/Dubai + USD 1.75/bbl

Geopolitics: Middle East

- Australia, New Zealand and Canada issued a joint statement that they are gravely concerned by indications Israel is planning a ground offensive into Rafah which would be catastrophic, while it was added that an immediate humanitarian ceasefire is urgently needed.

Geopolitics: Other

- US informed Congress and European allies of new intelligence regarding Russian nuclear capabilities although they do not pose an urgent threat to the US and are related to attempts by Russia to develop a space-based weapon, according to sources cited by Reuters.

- US Treasury Secretary Yellen said Russian President Putin will continue to threaten other countries if the US is not supportive of Ukraine, while she urged US House members to approve the supplemental funding bill with aid for Ukraine and said US national security is at stake. Furthermore, she said Trump's remarks on NATO and Russia were highly irresponsible and could undermine national security.

- Japanese Chief Cabinet Secretary Hayashi said North Korea is strengthening surprise attack capabilities by launching missiles from various platforms such as from submarines to trucks, according to Reuters.

US Event Calendar

- 08:30: Jan. Import Price Index YoY, est. -1.3%, prior -1.6%

- Jan. Import Price Index MoM, est. 0%, prior 0%

- 08:30: Jan. Export Price Index YoY, prior -3.2%

- Jan. Export Price Index MoM, est. -0.1%, prior -0.9%

- 08:30: Feb. Initial Jobless Claims, est. 220,000, prior 218,000

- Feb. Continuing Claims, est. 1.88m, prior 1.87m

- 08:30: Jan. Retail Sales Advance MoM, est. -0.2%, prior 0.6%

- Jan. Retail Sales Ex Auto MoM, est. 0.2%, prior 0.4%

- Jan. Retail Sales Control Group, est. 0.2%, prior 0.8%

- 08:30: Feb. Philadelphia Fed Business Outl, est. -8.1, prior -10.6

- 08:30: Feb. Empire Manufacturing, est. -12.5, prior -43.7

- 09:15: Jan. Industrial Production MoM, est. 0.2%, prior 0.1%

- Jan. Manufacturing (SIC) Production, est. 0%, prior 0.1%

- Jan. Capacity Utilization, est. 78.8%, prior 78.6%

- 10:00: Dec. Business Inventories, est. 0.4%, prior -0.1%

- 10:00: Feb. NAHB Housing Market Index, est. 46, prior 44

- 16:00: Dec. Total Net TIC Flows, prior $260.2b

Central Bank speakers

- 13:15: Fed’s Waller Gives Remarks on Dollar’s International Role

- 19:00: Fed’s Bostic Speaks on Outlook, Policy

DB's Jim Reid concludes the overnight wrap

The last 24 hours have been surprisingly calm after the turmoil of the previous session. 2yr US yields rallied back -8.0bps after rising +18.3bps the day before, encouraged by some dovish Fed speak. 10yr yields fell -5.8bps after the +13.5bps spike the previous session while December 2024 Fed pricing increased +8.9bps after a full 25bps had been taken out on Tuesday. The S&P 500 closed +0.96% higher, retracing nearly three-quarters of Tuesday’s losses.

Today we have a busy day of US data with retail sales the highli ght. So we will see if that continues to encourage volatility ahead of an important US PPI tomorrow, as some of its subcomponents inform forecasts for the core PCE number later this month. As Chicago Fed President Goolsbee reminded markets yesterday, the Fed’s inflation goal is based on the core PCE number, and not CPI. In addition, some of the strong services CPI drivers we saw in Tuesday’s print do not enter the PCE calculation and are instead taken from the PPI. A known dove, Goolsbee also stated “inflation can be [a] bit higher and still on track to 2%” and that he does not “support waiting until inflation at 2%” before the Fed cuts.

Whether he represents the views of the rest of the committee is open to some debate given his dovish history but for yesterday it was enough to calm the market to some degree as an additional +8.9bps of cuts were priced in by the Fed’s December meeting and we saw a notable -8.0bps and -5.8bps rally in 2 and 10yr yields. But there was little change in the market’s expectation of the timing of the first cut, with the first full 25bps still priced in for the June meeting.

Over in Europe, markets also modestly raised their expectations of ECB rate cuts, with +5.8bps more of cuts priced in by year-end. 10yr bund yields fell -5.7bp s, while OATs (-6.5bps) and BTPs (-9.0bps) outperformed.

In US equities, the S&P 500 rose by +0.96%, reversing much of Tuesday’s -1.37% decline and closing back above the 5,000 mark. The Russell 2000 (+2.44%) was the outperformer after the rout the day before that saw it experience its worst day (-3.96%) since June 2022, when the Fed made a late surprising move to guide the market to a 75bps hike. The NASDAQ rose +1.30%, with the Magnificent 7 (+1.53%) effectively erasing their -1.54% decline the previous day. A notable milestone was Nvidia (+2.46%) overtaking Alphabet’s (+0.55%) market capitalisation, to become the third largest company at $1.825trn. This comes only one day after the semiconductor company topped Amazon (+1.39% yesterday). Nvidia’s rise spearheaded a rally for the wider semiconductor sector, as the Philadelphia Semiconductor Index gained +2.18%. My CoTD yesterday discussed what happened next to all the top 5 companies in the S&P 500 over the last 60 years. See it here for more.

In the Eurozone, in terms of data we had the second print of Q4 GDP. As is typical, this was confirmed at the stagnant (0.0%) flash reading, but the details pointed to still solid (+0.3% qoq) employment growth in Q4. We also had the December industrial output, which posted at +2.6% month-on-month (vs -0.2% expected), but this upside was mostly due to distorted Ireland data. Against this backdrop, the STOXX 600 climbed +0.50%.

After the strong beat in US inflation on Tuesday, the downside surprise in UK CPI for January was a support for market from the early stages in Europe. UK CPI rose 4.0% year-on-year (vs 4.1% expected), and core by 5.1% (vs 5.2% expected).Services inflation rose 6.5%, lower than both consensus estimates (6.8%) and the BoE’s expectations (6.6%). But this is still a tenth higher than December’s print, and BoE’s Bailey confirmed yesterday this result is “not compatible with 2% target”. Yields on 10yr gilts still fell -10.5bps and the FTSE 100 rose +0.75%. Shortly after you read this, we will have the results of the Q4 GDP report for the UK. Our UK economist expects the UK slipped into a marginal technical recession in the second half of last year. Read the preview here.

Overnight in Asia, we had the preliminary Japanese Q4 GDP results, which came in below expectations at -0.4% quarter-on-quarter (vs 1.1% expected), up from -2.9% in Q3. See our economist's thoughts on the number here. There is now a high likelihood Japan is in a technical recession, and markets pared back expectations of rate hike bets, with the expected probability of a 10bps hike by April falling from 73% to 69%. Japanese equities were little fazed, with the Nikkei 225 up +0.96% as I type with a weaker Yen and tech driving the gains.

The Hang Seng index is also enjoying the risk-on sentiment, rising +0.43%. The Taiwanese TAIEX is up +2.78% as I type, having briefly touched an intraday record high, supported by an increase in the share price of semiconductor juggernaut Taiwan Semiconductor Manufacturing Co (+8.00%). Elsewhere, the Korean Kospi is trading down -0.15%. US equities futures are flat, whilst 10yr Treasury yields are down a further -2.0bps in the Tokyo session.

Briefly on commodities, US crude oil inventories rose by 12.02mn barrels, the greatest increase since December, and the second consecutive week of gains. This sent Brent crude tumbling -1.41% to $81.60/bbl yesterday after previously trading up on the day. WTI crude fell -1.58% to $76.64/bbl. Both are down an additional third of a percent this morning.

Finally to the day ahead, in terms of US data we have January retail sales, industrial production, capacity utilization, February Philadelphia Fed business outlook, NAHB housing market index, Empire manufacturing index, December net TIC flows, business inventories and weekly jobless claims. Elsewhere, we get UK Q4 GDP, Eurozone December trade balance, Canada January housing sales and December manufacturing sales. We will be hearing from the ECB’s Lane and Nagel, and the BoE’s Greene and Mann. Finally, earning releases include Applied Materials, Deere, Stellantis, DoorDash, DraftKings, and Roku.