The UK and Japan slipping into mild technical recessions with today’s GDP releases is an opportune moment to underscore that, while such developments may generate a lot of headlines, they have no forward-looking information content for investors. In fact, technical recessions typically precede rising asset returns.

Both the UK and Japan’s GDP contracted in the last quarter (ex any future revisions), after also contracting in the quarter before that, meaning both countries now satisfy the technical recession definition.

[ZH: Japan is even more divergent...]

There are two main problems with this categorization:

1) it is overly simplistic. There is little to no difference between an economy that contracts at 0.2% one quarter and is flat the next (no recession), and one that sees growth fall by 0.1% two quarters in a row (recession).

And 2), GDP is a lagging indicator. It is telling you where the economy was, not where it is going. Markets are forward-looking, and thus investors need focus their energies on leading indicators of the economy rather than GDP. Some information content can be gained by gauging the composition of growth, but there is nothing in a GDP report that will give any indication of an approaching turning point, where markets typically see their biggest moves.

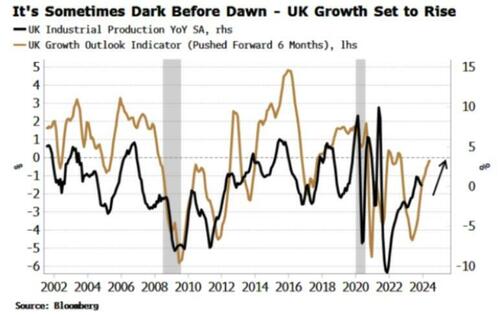

When it comes to the UK, leading indicators are rising, suggesting the worst could have already have passed for the economy.

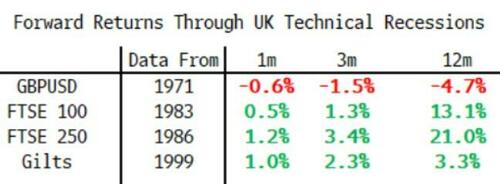

If we look at past technical recessions, they typically lead to falling gilt yields, and lower sterling.

That helps the FTSE 100 and FTSE 250 to perform well in the ensuing months.

It’s similar in Japan. The yen and JGB yields fall in the shorter term.

The Nikkei treads water in the short term after a technical recession, but after 12 months it returns an average of 10.7%.

The US is nowhere near a technical recession at the moment, but there too they on average mean positive returns, with the dollar, S&P and USTs all rising over the next one, three and 12 months.

Technical recessions generate a lot of heat, but not much light, and are little more than a distraction for investors.